Australian health insurers: From payers to providers

Australia's major private health insurers are no longer just paying claims. They're building clinics, acquiring platforms, backing startups, and in some cases competing directly with the hospitals they fund. The shift from payer to care provider is real, it's accelerating, and each fund is doing it differently.

This piece maps what each of the five major funds actually owns, who they partner with, where they're investing, and where the market gaps still are.

Five models, not one

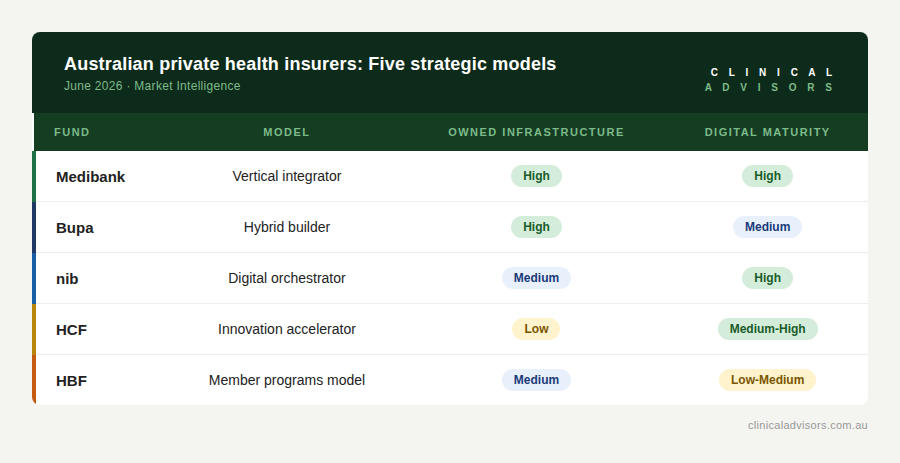

The temptation is to look at these funds as a group doing roughly the same thing. They're not. What's emerging is five meaningfully different bets on where health insurance value will come from over the next decade.

Medibank is the most vertically integrated: owning GP clinics, virtual care, hospital-at-home, aged care, and chronic disease management. Bupa has the broadest physical footprint and is rolling out an owned mental health clinic network at scale. nib is building a data-driven care orchestration layer through platform acquisitions. HCF ran the most active healthtech accelerator in the country before closing it. And HBF is transitioning from a WA-focused insurer into a care provider, slowly but deliberately.

The summary table below captures where each fund sits today.

HCF - Innovation Accelerator

HCF owns and runs HCF Dental Centres and HCF Eyecare Centres. Beyond that, its service delivery model is partner-heavy.

Key partner programs include GP telehealth via GP2U, second opinion and specialist assessment services through mlcoa (part of MedHealth), heart and diabetes health checks with the Victor Chang Cardiac Research Institute, skin cancer screening via MoleMap, telehealth psychology through PSYCH2U, online CBT programs for anxiety, depression and chronic pain via This Way Up, and a free 12-month Sleepfit subscription for eligible members.

HCF previously held a ~15% stake in GP2U, acquired in 2016 and subsequently sold. GP2U is now owned by My Emergency Doctor.

On the digital side, HCF built HCF Healthful, a proprietary member app with a personalised health score, goal tracking and community features.

The most significant activity was the HCF Catalyst healthtech accelerator, which ran for several years and produced one of the strongest startup alumni networks of any Australian health fund before closing. Alumni spanned telehealth (MyHealth1st, Medipass - now Tyro Health, myBeepr, Episoft,Pack & Pop, Chology, HealthLaunch), mental health and wellbeing (MindFit - now owned by Spectrum Life, SleepFit, Soldier.ly, Freedom From Chronic Pain, Agora, Family HQ), women's health (She Births, Birth Beat, The Pelvic Expert), digital therapeutics and chronic disease (CancerAid - now Osara Health, Perx Health, Cardihab, Techfit, Chemo@Home), diagnostics and screening (Nurochek, Skin Check Champions), aged care (Billy - acquired by ECH, Conpago), medical education (Vantari VR, Meksi), and clinical workflow tools (Scrubit, Consentic).

HCF built the strongest startup pipeline of any Australian insurer, but it has the least direct ownership of care delivery relative to peers. It functioned as an industry testbed: many Catalyst alumni have since been adopted by competitors. The accelerator is now closed, but its influence on the sector is still visible, as is their relentless Spotify adverts every time I go to listen to some tunes (albeit some of the above companies are now defunct).

Medibank - Vertical Integrator

Medibank owns and operates Amplar Health (covering virtual care, hospital-at-home, aged care at home, chronic disease management, and mental health services), myhealth Medical Centres, and Better Medical, two separate GP clinic networks.

Partner programs include cancer survivorship and support via Osara Health, PTSD care through Emyria, and digital chronic disease prevention and behavioural health programs through Amplar Health's partnership with Amwell and SilverCloud.

On the investment and acquisition side, Medibank acquired Medinet (a telehealth platform) and holds minority stakes in seven private hospitals. It also works with League for member engagement and digital health, and Engage People for its Live Better loyalty platform.

Proprietary digital products include Find Your Rhythm (a women's health app, now defunct?) and the Live Better digital prevention programs, which include Back Smart and Heart Wise.

Medibank is the fund most aggressively moving from insurer to healthcare operator. It owns the full stack: GP clinics, virtual care, hospital-at-home, aged care, and chronic disease management. No other Australian insurer currently has this level of direct control over care pathways.

Bupa - Hybrid Builder

Bupa owns and runs more care infrastructure than any other fund in Australia: Bupa Medical Centres, Bupa Aged Care (homes and nursing homes), Bupa Dental Centres, Bupa Optical, Bupa Medical Visa Services, and Mindplace - a mental health clinic network targeting around 60 sites by 2027, which is open to all Australians, not just Bupa members.

Partner programs include GP telehealth and chemist delivery via Blua (whitelabelled through Hola Health), hearing services through Amplifon, no-gap inpatient cardiology with Advara HeartCare (Australia's largest private cardiology group, with 120+ cardiologists across 60+ locations), and a free annual online CBT course for members via This Way Up.

Through Bupa Ventures, the fund has invested in Eugene (genetic screening), Vively (continuous glucose monitoring and lifestyle coaching), and Umps (remote in-home monitoring).

Bupa's Connected Care strategy explicitly targets integration across GP, dental, optical, mental health, and aged care. Mindplace is the single most significant new owned care asset to enter the Australian market in recent years, and Blua is the digital integration layer tying it together.

And they are definitely shouting about it. Blua by Bupa was the ‘Official Healthcare Partner and Digital Health Partner’ of the Australian Open 2026.

nib - Digital orchestrator

nib owns nib Dental Care, Honeysuckle Health (a population health analytics and care management business it acquired), and hub.health (a GP telehealth platform it acquired).

Partner programs cover symptom checking via Infermedica, cardiac rehabilitation through Cardihab, audiology with Specsavers, and digital mental health care through SilverCloud Health. In 2021, nib partnered with Snug Health to provide members with a digital health record.

The Honeysuckle Health and hub.health acquisitions signal a clear strategic orientation toward data-driven care orchestration over physical infrastructure. Honeysuckle brings population health analytics and care program capability. hub.health brings owned GP telehealth. Together they form a digital-first care navigation layer that is lighter on bricks and mortar and heavier on platform. They even won the ‘WeMoney Digital Health Insurer of the Year 2025’.

HBF - Member Programs Model

HBF owns and operates HBF Dental Centres (10 Perth metro locations, managed by Pacific Smiles, in which HBF holds a part-ownership stake) and its Life Ready physio network (acquired in 2022), which includes Life Ready Physio + Pilates clinics across WA and Victoria, Life Ready Mobile for in-home physio, and Life Ready Biosymm for workplace health and early intervention.

Partner programs include HBF Mind Matters (a post-hospitalisation mental health recovery program delivered through Mind Australia), hip and knee osteoarthritis management via the GLA:D program, telephone-based chronic disease coaching for CVD, diabetes, and COPD through The COACH Program, a 12-week online weight management program through the CSIRO Total Wellbeing Diet (via Digital Wellness), and chemotherapy at home through chemo@home. HBF was the first health fund in Australia to partner with chemo@home.

The headline digital health move is HBF Ventures, a $25 million corporate venture capital fund managed by Artesian, targeting 15 to 20 investments in digital health tools, new care models, and preventative health technologies over 10 years.

On the operational side, HBF made its first move into member-facing AI in mid-2026, deploying a Salesforce AgentForce agent to its 1.2 million members. The first phase is an unauthenticated web agent limited to general product and policy questions, with an authenticated version, able to recognise the member and actually do things like update contact details or surface claims information, slated to follow within months, and voice flagged as the step after that. Behind the scenes, HBF had already rolled the same generative tech out to all 200 of its contact-centre staff after a December pilot, reporting an 8% drop in average call-handling time and a 30% reduction in customer hold time. It is worth being precise about what this is: HBF is digitising the insurance side, service, claims, member admin, rather than the care-delivery side. That is consistent with its position as the least vertically integrated of the five funds, automating the payer while still partnering out the provider.

HBF is the most WA-centric fund on this list, still heavily reliant on external clinical programs for health management. The 2026 AgentForce rollout shows it executing on the digital service layer, but on the care side HBF Ventures still represents intent more than delivery. Of all five funds, HBF is the one most likely to accelerate through strategic partnerships or acquisitions over the next three years.

White space: what no fund is doing well

Despite significant activity, several meaningful gaps remain across the market:

GP telehealth at scale

No fund owns a dominant GP telehealth platform. Medibank acquired Medinet but it remains low-profile. nib's hub.health acquisition is the most credible play. Most funds still rely on third-party GP telehealth partners.

Mental health delivery

Mental health support is heavily partner-dependent across all five funds. Bupa's Mindplace is the first serious move into owned mental health clinic infrastructure. The rest rebate external psychology or fund third-party programs. This gap is already attracting global attention: in March 2026, Ireland-based Spectrum.Life entered the Australian market by acquiring three local digital mental health platforms - MindFit at Work, We Lysn, and Valion Health. The consolidation of the local vendor landscape by offshore players signals that the window for funds to establish owned or exclusive mental health delivery is narrowing.

Aged care (outside Bupa)

Aged care is almost entirely Bupa's domain. No other fund has made a meaningful move into aged care ownership or management. Given Australia's ageing population and the ongoing reform agenda, this remains an open lane.

Pharmacy

HBF has the most explicit pharmacy partnerships (Pharmacy 777 and TerryWhite Chemmart) but no fund has built a meaningfully integrated pharmacy capability. The interface between health insurance and medication management is underdeveloped across the board.

Women's health

HCF Catalyst had the deepest alumni base in women's health, and Medibank launched Find Your Rhythm (which now looks defunct), but no fund has a comprehensive owned women's health proposition.

Preventive health at the primary care interface

Most fund programs activate after a diagnosis or hospital admission. Pre-disease lifestyle and risk management, particularly around chronic disease prevention, is underfunded and fragmented. Medibank's Live Better programs and Amplar's Amwell-powered prevention tools are the most serious attempts.

Terry Cornick is a healthtech strategist and the founder of Clinical Advisors. This analysis draws on publicly available information and company announcements current as of June 2026.