Australian healthtech capital FY26: Where the $2.794B went by category

Australia deployed nearly $2.8 billion into healthtech in FY26, over 62 recorded transactions, but the capital didn't spread evenly. One mega-deal warped the landscape, while entire sectors were left behind.

The Eucalyptus effect

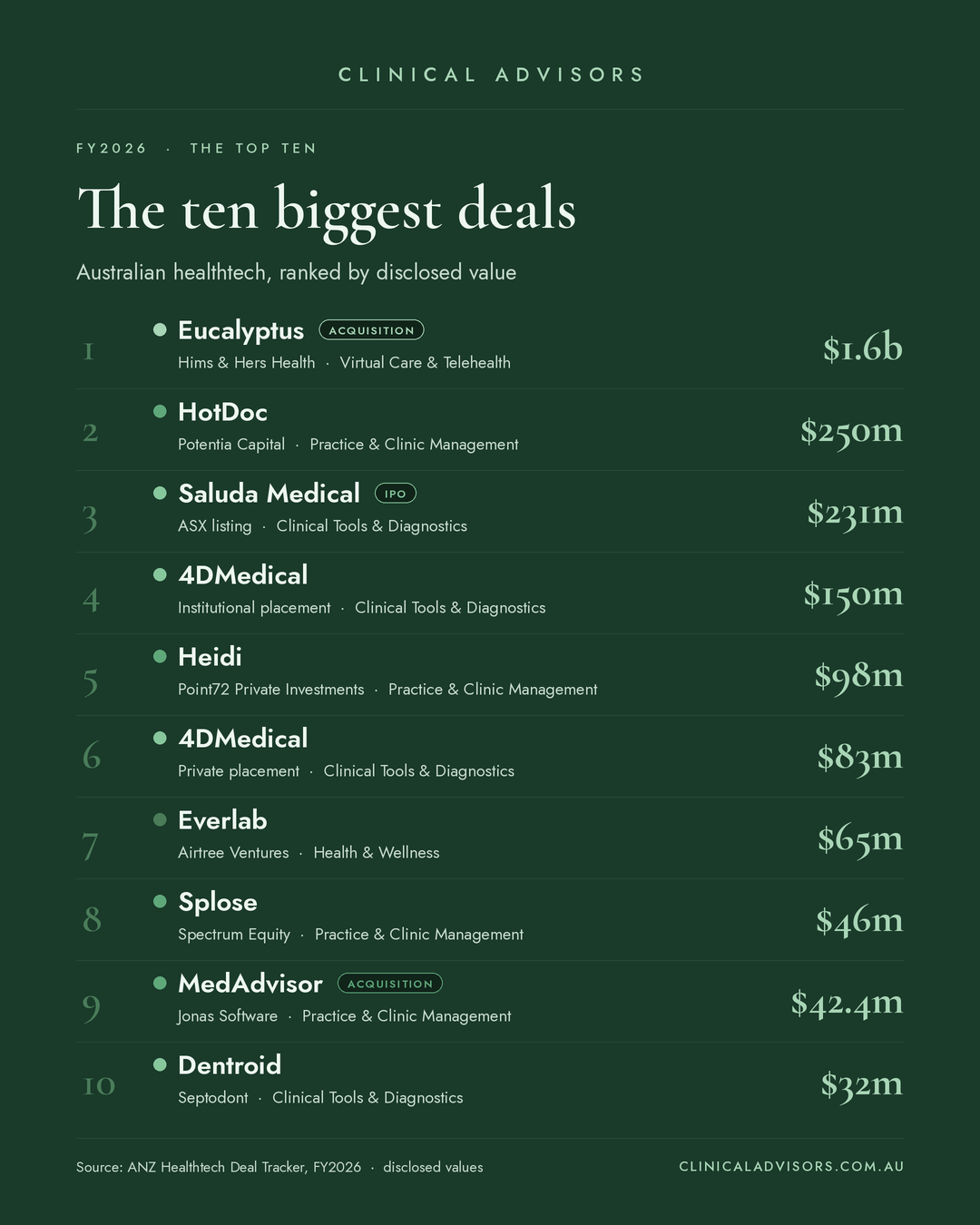

Hims & Hers paid $1.6 billion to acquire Eucalyptus, a digital health platform. That single transaction accounts for 57 percent of all measurable healthtech capital for the year. Strip it out, and you're looking at roughly $1.2 billion across everything else. The headline number is real, but the story underneath is different.

Where the actual capital went

After Eucalyptus, clinical tools and diagnostics claimed 21.8 percent of capital ($609 million). This is the substance play. Respiratory imaging (4DMedical, $233 million across two rounds), cancer diagnostics (Lumonus, OncoRes, AlleSense, Omniscient), maternal health monitoring (HeraMED, Oli), and neurotech (Saluda Medical, $231 million for an ASX listing) show market confidence in specialised tools for clinicians. These companies are solving real workflow problems for hospitals and specialists.

Practice and clinic management grabbed 14.1 percent ($395 million). HotDoc's $250 million Series B and Heidi’s $98 million from Point72 confirm that boring, profitable software still attracts large cheques. These platforms handle scheduling, billing, clinical workflows and integrations. They're not sexy but they're essential infrastructure.

Health and wellness picked up 5.1 percent ($143 million). Everlab (longevity), Bodd (fitness tracking), Hapana (gym software), and mental health platforms (Refresh, Tala Thrive) all found backing. This category grew with the addition of Andromeda (AI robotics) and Human Health, showing that consumer-facing wellness and preventive health remain investable.

Patient engagement and experience platforms managed just 1.6 percent ($45 million). MedAdvisor leads here with $42.35 million, a pathology platform turned engagement tool acquired by Jonas Software. This is tight capital allocation on a sector that should arguably be larger.

The glaring gaps

Four categories registered zero capital deployment in our FY26 dataset: ePrescribing and referrals, workforce and HR solutions (rostering, burnout support, credentialing), education and training (CPD, simulation, clinician compliance), and analytics and financial tools (claims processing, medical coding, BI dashboards).

These aren't niche concerns. Every practice needs roster and billing software. Every clinician needs CPD. Referrals and eScripts are foundation-layer infrastructure. Their absence from FY26's major deals suggests either that capital is being allocated quietly in tiny amounts, or that these categories are underserving investor expectations of growth and exit multiples.

The takeaway

FY26 shows Australian healthtech capital concentrating in imaging and diagnostic AI on one end, and defensive practice management on the other. Virtual care consolidated. But entire categories went unfunded in the major deal data. If you're starting or scaling a company in ePrescribing, workforce software or clinician education, you're operating in a capital gap. That gap represents opportunity or a warning signal depending on how you read it.

The data shows FY26 was a year of consolidation and conviction plays. Diagnostic AI works. Practice management pays. Virtual care de-risks with large acquisitions. Everything else is either bootstrapped, venture-backed quietly, or waiting for the next cycle.

Want to know where your opportunity sits in this capital map? Or access to the full list of deals? Reach out, we help healthtech founders and investors cut through the noise - terry@clinicaladvisors.com.au